- Emerging Markets Newsletter

- Posts

- Emerging Markets Newsletter

Emerging Markets Newsletter

Edition #2

Emerging Markets Network

September 02, 2024

Semester 2 Week 7

Hey Legend!

Happy Monday! Hope you’re doing well with midsems and assignments 💚. Welcome to the second edition of the Emerging Markets Newsletter !!!! 🥳

We have some exciting announcements to make 🥳. We will be running a pop-up stall 🏪 at the FBE Student Brunch this Thursday from 11.00 AM to 12.30 PM @ the Student Lounge in the Spot— come by and say hi!

Next Friday 13th Sep we have a FREE Coffee Catchup ☕️ @ Mid Square Coffee from 12.00 PM to 3.00 PM. Enjoy a cuppa on us and celebrate the conclusion of midsem season 😌, we can’t wait to see you there !!!! 😁

Keep an eye on our socials for further details, we will you updated. Now let’s get into the meat and potatoes of this week 🍽️.

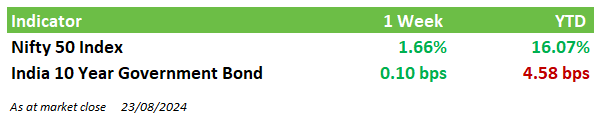

The Numbers

The Roundup

This week in the roundup we examine active Indian government expenditure 💸, mixed Chinese market performance 😳and escalations in the Middle Eastern war 🤼 which has the potential to shake up global markets 🌐

India

This week, we take a look at an exciting new social initiative from the Indian government 📚, a slowdown in economic growth 😔, policies targeting the small business sector 🏦 and developments in regional tensions 🗺️.

The Indian government has launched the National Digital Library 📚, offering free access to over 100 million digital books and educational resources 🏫. This initiative aims to close the educational gap 🎓, especially in rural areas, as part of the broader Digital India campaign.

India's Q1 FY25 GDP growth was 5.5%, with slowdowns attributed to Lok Sabha elections and a 1.2% contraction in the agricultural sector🚜. The government plans to increase the Dearness Allowance by 3% 📈 for its 11 million employees, addressing the current 6.3% inflation rate 📊 and aiming to boost domestic consumption.

New tax incentives have been introduced for startups and SMEs 🚀, including 100% tax exemption for the first three years and a $1 billion Venture Capital Fund 💰 to support sectors like AI and renewable energy. These measures have driven the BSE Sensex up by 2.4% 📈 in the past week, particularly benefiting technology and financial stocks.

India is enhancing its geopolitical influence with a $10 billion trade agreement 🤝 with Indonesia and increased joint military exercises with ASEAN nations. This is part of a strategy to strengthen ties in the Indo-Pacific region 🌏 and counter China's presence. Meanwhile, India is bolstering its border security with advanced deployments 🛡️ amid ongoing tensions with China and Pakistan.

China

This week, we examine Chinese carmaker BYD’s success ⚡️, growth in China’s high-tech industry🔬, the latest profit figures for China’s biggest lenders 🏦, and the latest in tariff tensions with Canada 🚢.

China’s biggest carmaker, BYD, reports a 24% profit increase during the first half of 2024📈. This is despite EV 🔋demand faltering domestically due to Chinese consumers reigning in consumption spending🛍️📉. BYD’s highly competitive pricing🏷️has enabled it to expand its market share abroad🌎, boosting revenues and compensating for domestic struggles.

China has boosted industrial 🏭 profits by 4.1% YOY, spurred by a 12.8% growth in high-tech manufacturing ⚡️🧑🏭 profits. High-tech manufacturing includes production of batteries🔋, semi-conductors and related products 📲💻. This has spurred confidence that China’s macroeconomic policies are beginning to support economic growth, however, analysts say the government now needs to act on boosting economic demand, rather than supply.

4 of the 5 biggest Chinese banks are reporting lower quarterly profits 🏦💰🔻. This is likely the result of various government initiatives and directives which aim to reduce the cost of borrowing in order to stimulate greater consumer spending 💸. Further, all 5 banks announced interim dividends, in line with recommendations from the country’s securities regulator⚖️, aiming to stabilise markets and boost investor returns 🤑👨💼.

Canada has announced a 100% tariff on Chinese-made EV’s🚙🔋, following similar announcements made by the EU and the USA. Notably, the tariff also impacts Tesla, which produces many of its cars in Shanghai, resulting in the company’s shares closing down by 3.2% 📉on the day of the announcement. Canada also simultaneously announced a 25% tariff on Chinese steel 📏.

Hot Topic 🔥

On August 25th, Hezbollah, the Lebanese militant group, launched an attack on Israel, retaliating for the assassination of one of its senior commanders, Fu’ad Shukr, in July.

While the U.S. intelligence community assesses that Hezbollah does not currently intend to escalate this into an all-out war, the group's choice of military targets in Sunday’s airstrikes appears to be a calculated response, likely intended to signal a measured approach.

There are rising concerns that Iran may respond to the Israeli killing of a top Hamas official in Tehran, potentially triggering further attacks from other Iranian-backed groups. Concurrently, the ongoing conflict in Gaza, with its increasing Palestinian death toll, shows no signs of settling. The key negotiators—Hamas leader Yahya Sinwar and Israeli Prime Minister Benjamin Netanyahu—are currently far from reaching any resolution, increasing the risk of spillover into a broader regional war, potentially drawing in neighbouring states and the United States.

Financial markets reacted swiftly to these developments. On August 25th, key Tel Aviv share indices rose ~2%, with the blue-chip index Tel Aviv 35 hitting a record high. This surge followed an Israeli pre-emptive strike against Hezbollah, which successfully prevented a potential rocket barrage on key Israeli targets. The Tel Aviv 35 index closed 2% higher after reaching an intra-day peak of 2091.91, while the broader TA-125 index gained 2.1%.

According to Yuval Tzuk, an economist in the bourse's research department, the trading day started positively following the Air Force’s successful pre-emptive strike. Additionally, the share gains were supported by growing expectations of U.S. interest rate cuts, which provided further market optimism.

If the conflict were to fire up, its impact would reverberate beyond the region.

Historically, geopolitical tensions have led to declines in equity markets, as investors shift to safe-haven assets like gold and government bonds, negatively affecting stock prices. Companies with significant exposure to the Middle East will see their valuations adversely impacted.

The Middle East is a crucial player in global oil production. Prolonged conflict in the region could disrupt key shipping routes, such as the Strait of Hormuz, leading to a spike in oil prices. This could, in turn, drive up global inflation rates and destabilise economic conditions worldwide.

Geopolitical instability often leads to appreciation in safe-haven currencies like the U.S. dollar, Swiss franc, and Japanese yen, while EM currencies may depreciate due to increased perceived risks. This could distort currency markets, reverberating onto global trade and investment flows.

Have a good rest of the week, we hope to see you at our upcoming events 🤝

Best regards,

EMN 💚